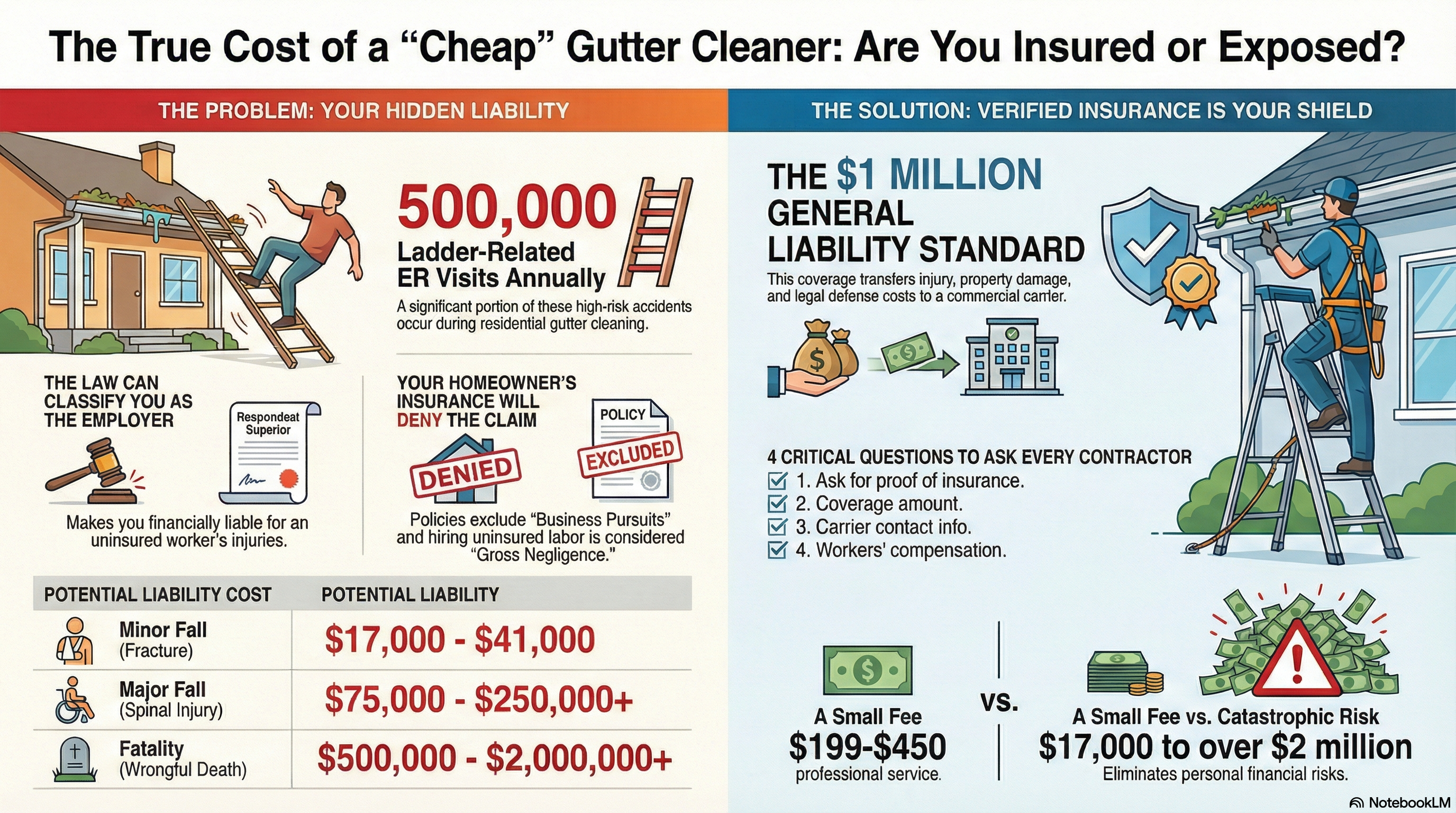

Homeowners who hire uninsured contractors for gutter cleaning face personal liability exposure for the 500,000 annual ladder-related emergency room visits documented by the Consumer Product Safety Commission.

Standard homeowner insurance policies often exclude coverage for "Business Pursuits" or classify hiring unlicensed labor as "Gross Negligence," denying claims when uninsured workers sustain injuries on your property. Medical treatment costs for ladder-related fractures range from $17,000 to $41,000, with emergency room triage alone averaging $2,600 before any diagnostic imaging or orthopedic consultation.

Professional gutter cleaning services maintain minimum $1 million general liability coverage, transferring injury risk from homeowners to commercial insurance carriers. Clean Pro's network requires verified proof of active insurance from all independent service providers, with quarterly renewal checks ensuring continuous coverage protection.

Verify Insurance Coverage Before Booking →The Legal Doctrine Homeowners Don't Know About

Respondeat Superior (Latin for "Let the Master Answer") establishes homeowner liability when directing contractor work or providing equipment to unlicensed workers. Courts classify homeowners as the "employer of record" under Respondeat Superior doctrine, creating personal financial exposure for on-site injuries regardless of contractor self-employment status.

The precedent case Heiman v. Workers' Comp Appeals Board (2007) confirmed HOAs and property owners face full liability when hiring contractors without proper licensing or workers' compensation coverage. Insurance companies use this classification to deny homeowner policy claims, arguing that hiring unlicensed labor constitutes intentional risk-taking excluded from standard coverage.

The Real Cost of 500,000 Annual Ladder Injuries

The Consumer Product Safety Commission's National Electronic Injury Surveillance System (CPSC/NEISS) documents ~500,000 emergency room visits annually from ladder-related injuries, with approximately 300 fatalities per year. Gutter cleaning accounts for a significant portion of residential ladder accidents due to height requirements, unstable footing on wet rooflines, and repetitive positioning changes.

| Injury Type | Frequency | Treatment Cost | Homeowner Liability |

|---|---|---|---|

| ER Triage (No Admission) | Most Common | $2,600 | Personal Payment |

| Fracture Treatment | Common | $17,000 - $41,000 | Personal Payment |

| Spinal Injury | Moderate | $75,000 - $250,000+ | Personal Payment + Legal |

| Fatality (Wrongful Death) | ~300/year | $500,000 - $2M+ | Personal Assets at Risk |

Uninsured contractors lack workers' compensation coverage, shifting medical cost burden directly to homeowners under Respondeat Superior doctrine. Personal injury attorneys target homeowners with higher asset values, recognizing that contractor judgment-proof status makes property owners the only viable defendants.

How Insurance Companies Deny Homeowner Claims

Insurance carriers apply three specific exclusions when denying claims involving uninsured contractor injuries. Policy language varies by state and carrier, but these exclusions appear consistently across major providers.

1. Business Pursuits Exclusion

Hiring contractors to perform paid work on your property constitutes a "business pursuit" under insurance definitions. Carriers argue that homeowners engaging in commercial hiring transactions operate outside residential policy coverage scope, even for one-time service purchases.

2. Gross Negligence Classification

Insurance adjusters classify hiring unlicensed or uninsured labor as "gross negligence"—willful disregard for foreseeable harm. Gross negligence voids standard homeowner liability coverage, exposing personal assets to legal judgment without policy protection.

3. Employer Liability Exclusion

Policies exclude coverage for policyholders who assume employer responsibilities by directing work, providing equipment, or setting performance standards. Courts interpret contractor direction as employment relationship formation, triggering employer liability exclusions that void homeowner coverage.

"Clean Pro did a great job with my gutter cleaning. Their scheduling process was seamless, and they kept me informed on every step of the process. Highly recommended!"

— Eric Johnson, Kansas City, MO

The $1 Million Coverage Requirement Explained

Professional service providers carry $1 million general liability insurance as industry standard minimum coverage. General liability insurance protects against third-party bodily injury claims, property damage, and legal defense costs resulting from business operations.

Annual premium costs for $1 million coverage range from $796 to $1,230 for small trade businesses, with rates varying by claim history, service area risk factors, and coverage limits. Legitimate contractors build insurance costs into service pricing, while unlicensed operators undercut market rates by eliminating insurance expense—and transferring injury risk to homeowners.

What General Liability Insurance Covers

- Contractor injuries result from falls, equipment failures, or other on-site accidents during service delivery

- Property damage claims arise when cleaning processes damage roofing materials, fascia boards, or landscaping

- Legal defense costs accumulate from homeowner claims for incomplete or defective work quality

- Third-party injuries occur from falling debris striking bystanders, vehicles, or adjacent properties

Clean Pro's vetting process requires certificate of insurance verification through direct carrier contact, with quarterly renewal checks confirming continuous coverage. Homeowners receive insurance confirmation before booking finalization, eliminating coverage verification burden.

Real Property Damage Scenarios That Trigger Liability

Uninsured contractors create financial exposure beyond injury liability through inadequate work quality that causes property damage. Understanding water intrusion prevention protects against the $13,954 average water damage insurance claim documented by RubyHome and ISO statistics.

Foundation Damage from Improper Drainage

Clogged gutters allow hydrostatic pressure to build against foundation walls when water accumulates in soil adjacent to basement perimeters. Foundation piering to stabilize settling structures costs $1,500 to $3,000 per pier, with typical repairs requiring 5-10 piers ($7,500-$30,000 total project cost).

Basement waterproofing systems installation averages $3,000 to $10,000 for interior drainage solutions, with exterior excavation and waterproofing membrane application reaching $15,000-$30,000 for perimeter protection. Professional gutter cleaning prevents these costs by maintaining proper water diversion away from foundation substrates.

Ice Dam Formation in Winter Climates

Inadequate gutter cleaning before winter allows debris accumulation that blocks proper drainage when snow melts. Ice dam formation forces meltwater under shingles, causing attic insulation saturation, ceiling staining, and structural rot. Roof repair costs for ice dam damage range from $400 to $1,500 per affected section, with complete shingle replacement projects reaching $8,000-$15,000.

Uninsured contractors lack professional liability coverage for consequential damages, leaving homeowners to fund repairs from inadequate service delivery without recourse for contractor reimbursement.

How Clean Pro's Vetting Process Protects Homeowners

Clean Pro operates as a national booking agency connecting homeowners with vetted, insured independent service providers across 42 states. The vetting process transfers liability verification burden from homeowners to the booking platform through multi-step insurance confirmation.

Insurance Verification Protocol

Independent contractors submit proof of current general liability insurance during network application, with minimum $1 million coverage required for approval. Clean Pro's compliance team contacts insurance carriers directly to verify:

- Policy verification confirms active coverage status with no pending cancellations or non-renewal notices

- Coverage limits validate minimum $1 million general liability protection meets network requirements

- Renewal date tracking schedules quarterly re-verification checks to catch lapses before coverage expiration

- Additional insured status allows homeowners to request endorsement adding them as protected parties under contractor policies

Contractors with expired or lapsed coverage face immediate network suspension until proof of renewed insurance arrives through carrier verification. Homeowners receive insurance status confirmation in booking confirmations, with certificate of insurance copies available upon request.

"The man who cleaned our gutters seemed to be very thorough which we really appreciate. He cleaned the debris off our patio and it looks great! Thank you!"

— Alayne Leang, Taylors,, SC

What Uninsured "Cheap" Services Actually Cost

Unlicensed operators advertise rates 30-50% below market pricing by eliminating insurance costs, licensing fees, and equipment investments that legitimate contractors include in service pricing. Homeowners attracted to below-market rates assume risks worth 10-100x the savings.

| Scenario | "Savings" from Cheap Service | Potential Liability Cost | Net Risk Exposure |

|---|---|---|---|

| Minor Fall Injury | $75-$150 | $17,000 - $41,000 | 113x - 547x Loss |

| Spinal Injury | $75-$150 | $75,000 - $250,000 | 500x - 3,333x Loss |

| Fatality (Wrongful Death) | $75-$150 | $500,000 - $2M+ | 3,333x - 26,667x Loss |

| Property Damage (Foundation) | $75-$150 | $7,500 - $30,000 | 50x - 400x Loss |

Professional gutter cleaning costs between $218 and $470 for most residential homes, reflecting legitimate operating costs including insurance, fuel, equipment, and fair market wages indexed to BLS Code 37-3011 (Landscaping and Groundskeeping Workers). Attempting to save $75-$150 by hiring uninsured labor creates exposure to six-figure liability.

Get Instant Quote from Insured Provider →Questions to Ask Before Hiring Any Gutter Cleaner

Can you provide current proof of general liability insurance?

Legitimate contractors provide certificate of insurance copies showing policy number, coverage limits, effective dates, and carrier contact information. Verbal claims of insurance without documentation indicate likely fraud, as insured contractors maintain digital certificate copies for immediate customer verification.

What is your minimum coverage amount?

Industry standard minimum coverage stands at $1 million general liability, with many professional services carrying $2 million limits for additional protection. Contractors offering lower coverage amounts ($100,000-$500,000) signal inadequate risk management that may not cover catastrophic injury scenarios.

Can I contact your insurance carrier to verify coverage?

Requesting carrier contact information separates legitimate providers from fraudulent operators using fake certificates. Insurance carriers confirm coverage status, policy limits, and renewal dates when contacted directly, eliminating certificate forgery risk.

Do you carry workers' compensation insurance?

Sole proprietors without employees may legally operate without workers' compensation coverage in most states. Multi-person crews require workers' comp to protect employee injuries, with coverage absence creating homeowner liability exposure when crew members sustain injuries on your property.

What happens if you damage my property during cleaning?

General liability insurance covers property damage claims from fascia scratching, shingle damage, or landscape destruction during service delivery. Uninsured contractors lack financial resources to compensate property damage, forcing homeowners to fund repairs without contractor reimbursement recourse.

The Hidden Costs of DIY Gutter Cleaning

Homeowners attempting DIY gutter cleaning to avoid service costs face the same 500,000 annual ladder injury statistics affecting uninsured contractors. Personal injury from DIY accidents triggers medical costs, lost work income, and potential long-term disability without contractor liability insurance protection available when hiring professionals.

Ladder rental costs ($40-$75/day), safety equipment purchases (harness systems $150-$300), and debris disposal fees ($25-$50) reduce DIY cost savings while maintaining full injury risk exposure. For homeowners confronting the complete risks of DIY gutter cleaning including safety equipment requirements and OSHA ladder standards, professional service costs represent insurance premium payments against catastrophic injury.

Two-story homes require extension ladders reaching 24-28 feet, with OSHA Standard 1926.1053 requiring 4-to-1 angle ratios and rails extending 3 feet above landing points. Homeowners lack training in proper ladder positioning, creating fall risk from improper setup that professional contractors eliminate through daily repetition and safety protocol adherence.

Commercial Property Manager Liability Concerns

Property managers hiring contractors for HOA or commercial gutter cleaning assume fiduciary liability for tenant safety and building maintenance. The Heiman v. Workers' Comp Appeals Board (2007) case established HOA liability for unlicensed contractor injuries, with courts ruling that property managers owe tenants reasonable care duty including contractor vetting.

Commercial general liability policies contain similar "Business Pursuits" exclusions as residential policies, denying coverage when property managers hire unlicensed labor. Professional property managers require contractor certificate of insurance copies for liability transfer documentation, with additional insured endorsements naming management companies as protected parties under contractor policies.

Scam Prevention: Fake Insurance Certificates

Fraudulent contractors present forged insurance certificates showing false policy numbers, expired coverage dates, or non-existent carriers. Certificate forgery detection requires carrier verification through direct phone contact listed on certificate letterhead, with policy number confirmation and coverage limit verification.

Understanding common tactics used in scams to avoid when hiring gutter cleaners protects against fake licensing claims, pressure tactics, and deposit fraud. Legitimate contractors welcome insurance verification requests, while fraudulent operators resist carrier contact or provide disconnected phone numbers.

ACORD (Association for Cooperative Operations Research and Development) certificate forms contain security features including carrier-specific formatting, agent signature requirements, and standardized policy information fields. Homemade certificates printed on plain paper signal probable fraud, as licensed insurance agents issue official ACORD forms through carrier systems.

Uncommon Liability Scenarios

What if the contractor is injured but refuses medical treatment?

Injured contractors declining immediate medical treatment create delayed liability exposure when symptoms worsen days or weeks after the initial incident. Soft tissue injuries, concussions, and internal bleeding may not manifest until hours after falls, with contractors attributing later injuries to your property incident despite delayed reporting.

Uninsured contractors lacking medical coverage often delay treatment until injuries become severe, maximizing eventual claim amounts. Document all on-site incidents immediately with photos, witness statements, and written contractor confirmation of injury status, creating evidence trail for potential future claims.

Historic Properties with Specialized Insurance Requirements

Historic home insurance policies contain additional contractor requirements including historic preservation certification, specialized material handling training, and higher liability limits ($2-$5 million) due to irreplaceable component values. Standard $1 million coverage may prove insufficient for historic property damage claims involving custom millwork, original gutters, or protected architectural features.

Contractors working on National Register properties face liability for unauthorized alterations violating preservation standards, with homeowners sharing responsibility for contractor selection. Historic property owners require contractors to carry specialized historic restoration insurance endorsements covering preservation guideline compliance.

Shared Property Liability in Multi-Unit Buildings

Condo associations and multi-unit property owners hiring gutter cleaning services create shared liability exposure across all unit owners when uninsured contractors sustain injuries. HOA insurance policies may deny claims under business pursuits exclusions, forcing special assessments across all unit owners to fund injury settlements.

Condo declarations often require board approval for contractor hiring, with insurance verification mandatory before service authorization. Unit owners hiring private contractors without board approval violate governing documents and assume personal liability for injuries occurring in common areas.

Regional Insured Gutter Cleaning Service Coverage

Clean Pro's nationwide network connects homeowners with verified, insured service providers carrying minimum $1 million general liability coverage. Quarterly insurance verification checks confirm continuous policy status across all markets, transferring injury liability from homeowners to commercial carriers.

National Service Provider Verification Standards

Independent contractors in Clean Pro's network maintain active insurance policies with carrier verification before homeowner booking approval. Professional cleaning services operate in Atlanta, Boston, Charlotte, Chicago, Dallas, Denver, Houston, Nashville, New York, Philadelphia, Seattle, and St Louis, providing certificate of insurance copies and carrier contact information for homeowner verification before service delivery.

Request your 15-minute quote from insured professionals eliminating personal liability exposure from contractor injuries.

Related Home Safety & Risk Management Guides

Insurance and liability protection extends beyond gutter cleaning to comprehensive property risk management. Professional service providers in Clean Pro's network connect homeowners with specialists for related safety and prevention projects:

- Ladder safety statistics show 300 annual fatalities from falls, with 70% occurring during routine home maintenance. For complete analysis of injury patterns and prevention protocols, review the comprehensive breakdown of risks of DIY gutter cleaning including OSHA ladder standards and equipment requirements

- Foundation protection costs average $7,500-$30,000 for piering and waterproofing when hydrostatic pressure causes structural damage. Professional drainage prevents the $13,954 average water damage claim (analyze full water damage cost breakdown and prevention strategies)

- Ice dam prevention in northern climates requires pre-winter gutter clearing to prevent meltwater intrusion under shingles. Roof repair costs from ice dam damage range $400-$1,500 per section (understand ice dam formation mechanics and gutter connection)

- Contractor fraud detection protects against deposit scams, fake licensing claims, and pressure tactics that target homeowners. Verification protocols identify fraudulent operators before payment (review complete scam prevention checklist and red flag identification)

Professional gutter cleaning with verified insurance coverage costs $218-$470 annually—representing 1.4-3.2% of the $13,954 average water damage claim and eliminating six-figure personal liability exposure from uninsured contractor injuries.

Homeowners face personal liability for the 500,000 annual ladder injuries when hiring uninsured contractors. Standard insurance policies exclude "Business Pursuits" coverage, denying claims when unlicensed workers sustain injuries on your property. Respondeat Superior doctrine establishes homeowners as employers of record, creating financial exposure for medical costs ($17,000-$41,000 per fracture) and wrongful death settlements ($500,000-$2M+).

Clean Pro's network requires minimum $1 million general liability insurance from all independent service providers, with quarterly verification checks confirming continuous coverage. Homeowners receive insurance status confirmation before booking, transferring injury liability from personal assets to commercial carriers. Professional service costs ($218-$470) represent insurance premium payments eliminating catastrophic liability risk.

Get Insured Service Quote in 60 Seconds →